By Katerina V., payments content, covering crypto processing for iGaming and eCommerce operators.

Updated: 2026-07-07

A rolling reserve freezes a share of a merchant's own revenue as a standing hedge against future refunds and chargebacks, typically 5-10% of turnover held for 90-180 days, rather than because anything specific went wrong with a given transaction (TechBullion, "The Best High-Risk Payment Gateway in 2026"). For a high-risk operator running $2.8 million a year, a 10% reserve held on a rolling 180-day basis means roughly $140,000-$150,000 sits locked up at any given time, money unavailable for partner payouts, traffic spend, or product development.

This article explains why rolling reserve became standard in high-risk payment infrastructure, what it costs a growing business beyond the contract line item itself, and what specifically changes when settlement moves to crypto.

Rolling reserve: standard practice, real cash-flow drag

Rolling reserve is the mechanism where a processor holds back part of a merchant's revenue to cover possible future refunds and disputes, typically 5-10% of turnover, returned after 90-180 days. It hits hardest in digital goods, iGaming, subscription models, and cross-border eCommerce, the segments where processors apply reserves most often because of elevated chargeback, refund, and fraud-signal risk.

At $2.8 million in annual turnover, even a 10% reserve puts real pressure on cash flow: tens to well over a hundred thousand dollars can be out of circulation at any given time, and many processors don't disclose the exact percentage or release timeline until after the contract is signed, which makes financial planning harder than the headline rate suggests.

Why the market normalized rolling reserve

Risk perception. Processors place iGaming and digital goods in a higher risk category for refunds and fraud, and offset that classification by holding back part of turnover regardless of a specific merchant's actual dispute history.

Limited disclosure upfront. The exact percentage and release timeline commonly become clear only after signing, producing financial commitments that were difficult to plan for in advance.

Limited provider choice. Merchants in offshore jurisdictions often have relatively few processors to choose from, which increases exposure to whatever terms the available providers set.

No standardization. Unlike banking, crypto and high-risk card processing have no uniform reserve rules; percentages, hold periods, and release conditions differ meaningfully from one provider to the next, which makes comparing offers difficult without a common baseline.

| Factor | Why it's a problem for the merchant |

|---|---|

| Risk perception | 5-10% of turnover frozen as a precaution, independent of actual refund history |

| Limited disclosure | Exact percentage and timeline often become clear after signing, not before |

| Limited provider choice | Few alternatives; terms are largely accepted as given |

| No standardization | Difficult to compare providers on real reserve conditions |

Three types of operational damage, not just a fee

Cash flow. For an operator with $500,000 in monthly turnover, a 10% reserve held for up to 180 days can mean roughly $50,000 permanently out of reach at any point, pressuring liquidity in segments where cash needs to move quickly.

Reputation. Delays in paying partners and suppliers build a reputation for unreliability that isn't priced into the fee schedule at all; it shows up later as damaged relationships and, in an environment where negative reviews travel quickly, becomes a systemic risk of its own.

Operational time. Managing fund-release processes and reconciling transactions against reserve terms takes real finance-team effort, time that isn't spent on work that actually grows the business.

Why attempts to fix this at the negotiation table usually fail

Negotiating a lower reserve percentage often ends with higher fees or new charges added elsewhere in the contract, an especially heavy trade for merchants already paying above-market rates. Some operators try alternative payment systems hoping to cut costs and encounter a similar pattern: an attractive initial rate followed by additional charges introduced later that change the real economics, which both compresses margins and makes budgeting unreliable, since a plan built around one set of terms doesn't hold once those terms shift.

A related, often overlooked issue is the lack of transaction-level detail: without a full cost breakdown, an operator doesn't know the final fee amount until the invoice arrives, which turns a routine infrastructure decision into a forced, unplanned migration if the provider changes terms or exits the segment while the business is mid-growth.

What changes for crypto transactions specifically

Standard card processing uses rolling reserve to protect the processor against chargebacks, disputes, and refunds initiated through card networks. Pure crypto transactions don't generate card-style chargebacks in the first place, since there's no card network dispute process to protect against, which is why a rolling reserve on crypto settlement specifically is a policy choice by the provider rather than a structural necessity the way it is for card processing.

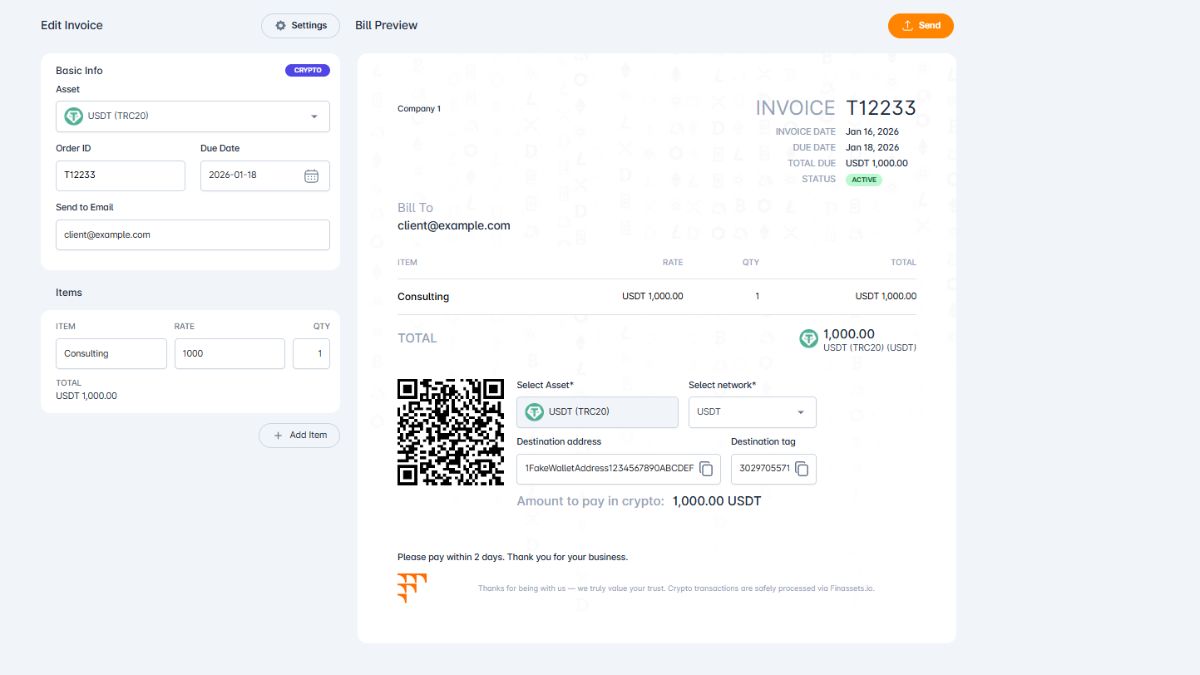

| Standard processor | Finassets |

|---|---|

| Rolling reserve 5-10%, held 90-180 days | No rolling reserve on crypto transactions |

| Terms and release timeline often clear only after signing | All fees fixed in the contract and visible in the dashboard before you start |

| Transaction detail shows a final amount with no breakdown | CSV export with separate columns: service fee, network fee, sweep fee, exchange fee |

| Network fee known only after the fact, depending on load | TRC-20 transaction cost known before confirmation, when Energy is available |

On the TRON network specifically, the standard TRX-burn mechanism produces a variable transaction cost that moves with the price of the native token; a direct burn transfer typically runs $1.60-$4.20 depending on wallet state (Eco Network, "USDT TRC-20 Fees 2026"). The TRON Energy Saving System addresses this by pre-purchasing Energy in bulk so the per-transaction cost is fixed before confirmation, with up to 50%+ fee reduction on network fees, depending on Energy availability and network conditions (based on client results; individual outcomes vary).

What crypto settlement adds beyond removing card-style reserves

Deloitte's 2026 merchant survey found 85% of surveyed merchants expect digital currencies to become mainstream in their industry within the year (Deloitte, "Merchants getting ready for crypto"). McKinsey and Artemis Analytics found actual stablecoin payment volume reached about $390 billion in 2025, more than doubling from 2024, once raw on-chain transaction volume (much of it internal transfers and trading, not payments) is filtered out (McKinsey, "Stablecoins in payments: What the raw transaction numbers miss"). On the institutional side, 86% of investors surveyed by EY-Parthenon and Coinbase in 2026 are already using or actively exploring stablecoins for internal cash management (EY-Parthenon/Coinbase, 2026 Institutional Investor Digital Assets Survey).

Checklist: evaluating a processor for eCommerce on reserve terms specifically

- Confirm whether all fees are fixed in the contract, including service fee, network fee, and sweep fee.

- Clarify whether the final transaction cost is known before payment or only after settlement.

- Confirm there's no minimum monthly turnover, hidden maintenance fee, or inactivity fee.

- Check whether a rolling reserve applies, and if so, what percentage and for how long.

- Confirm reserve release conditions are fixed in the contract, not decided case by case.

- Ask specifically whether rolling reserve applies to crypto transactions and stablecoin settlement.

- Confirm the support SLA on response time is fixed in the contract.

- Confirm support is available during payment incidents, not only standard business hours.

- Confirm the processor supports volume growth, API integration, and dual-run migration without renegotiating core terms.

- Confirm the provider's regulatory status and KYB process match your operating jurisdiction and licensing requirements.

Where this doesn't apply

None of this changes much for a business processing very low volumes, where even a 10% reserve is a small absolute number and the operational effort of switching providers may outweigh the benefit. It also doesn't apply where a business's revenue is genuinely at low dispute risk by the card network's own criteria, since reserves there tend to be smaller and more negotiable in the first place. And removing card-style reserve exposure through crypto settlement doesn't eliminate every operational cost: network fees, sweep fees, and provider-specific policies still apply and need the same contract-level scrutiny.

Finassets: crypto processing without a frozen share of turnover

Rolling reserve solves a real risk problem for the processor, but it does so by shifting the cost onto the merchant. For pure crypto transactions, that mechanism isn't structurally necessary, since there are no card-style chargebacks to protect against in the first place.

Finassets is a Panama-registered provider of crypto payment infrastructure for licensed iGaming operators, digital goods platforms, and other regulated high-risk businesses operating cross-border, crypto-driven models: no rolling reserve on crypto transactions, all fees fixed in the contract and itemized in the Back Office by service fee, network fee, sweep fee, and exchange fee, a CSV export with a full cost breakdown, the TRON Energy Saving System fixing TRC-20 cost before confirmation (subject to Energy availability), Telegram support with response-time targets fixed in the contract, support for operators licensed under recognised regimes (Curaçao, Anjouan, Kahnawake, and similar), and onboarding in 2-7 business days, subject to KYB and compliance review.

Start by measuring what's actually locked up right now

Rolling reserve isn't unavoidable for every business model. For high-risk segments with a crypto-native audience, crypto settlement removes the main mechanism that creates it in the first place. The useful next step is measuring exactly how much is sitting in reserve today and how the unit economics change with a different settlement setup.

Write to us and we will look at your current setup and calculate the real total cost of ownership.

FAQ

What is a rolling reserve, and why do processors use it? A rolling reserve is a percentage of a merchant's turnover, typically 5-10%, that a processor holds back for 90-180 days as a hedge against future refunds and chargebacks (TechBullion, 2026). It applies regardless of a specific merchant's actual dispute history, which is why it functions as a blanket risk offset rather than a penalty for anything the merchant did.

How much money does a rolling reserve actually lock up for a growing business? It scales directly with turnover and the reserve percentage. At $2.8 million in annual turnover with a 10% reserve held on a rolling 180-day basis, roughly $140,000-$150,000 sits locked up at any given time; at $10 million in monthly turnover with a 10% reserve, that figure runs closer to $1 million continuously frozen (iGaming Payment Solutions, 2026).

Does moving to crypto settlement automatically eliminate rolling reserve? Not automatically, but the structural justification for it weakens significantly. Card-style rolling reserve exists to cover chargebacks initiated through card networks; pure crypto transactions don't generate that type of dispute, so a provider applying a reserve to crypto settlement is making a policy choice rather than responding to a structural risk that doesn't exist on-chain.

Why do negotiations to lower a rolling reserve often backfire? Processors frequently offset a lower reserve percentage by raising fees elsewhere or introducing new charges, which can leave a merchant paying more in total even with a smaller reserve. This is a particular problem for merchants already paying above-market rates, since there's less room to absorb additional line items without the total cost rising.

Is there real evidence that switching to crypto settlement matters to merchants, not just processors? Yes, at a measurable scale. Deloitte's 2026 survey found 85% of merchants expect digital currencies to become mainstream in their industry, and McKinsey and Artemis found actual stablecoin payments reached about $390 billion in 2025, more than doubling from 2024 (McKinsey, 2026). Separately, 86% of institutional investors surveyed by EY-Parthenon and Coinbase in 2026 are already using or exploring stablecoins for cash management specifically.

What should a merchant check in a contract to avoid an unexpected rolling reserve? Confirm whether a reserve applies at all, and if so, the exact percentage, hold period, and release conditions, in writing, before signing. Also confirm whether that reserve applies specifically to crypto transactions and stablecoin settlement, since some providers apply card-style reserve logic to crypto flows by default even though the underlying chargeback risk doesn't carry over.