An iGaming operator in Latin America, Africa or Southeast Asia loses money not only on fees. Some losses come from settlement delays, weak local currencies, rolling reserve at the acquirer, declined card deposits and volatile crypto on the balance.

The problem is that money does not always reach the operator quickly in the right currency. While a payment moves through banks, the acquirer, reserves and FX conversion, the rate can change. If the operator accepts BTC or ETH and does not convert them in time, market risk is added on top of payment risk.

This article looks at exactly where these losses occur, which part of them stablecoins and auto-conversion can reduce, and where compliance obligations remain.

Settlement delays turn a payment problem into a currency risk

In emerging markets, money can lose value while settlement is still in progress. A payment may be approved, but the funds are still waiting for clearing, settlement or release from rolling reserve. If the local currency has weakened during that time, the operator gets less in real terms.

According to BIS (2025), only 35% of global retail cross-border payments are credited within one hour. The average global cost of a remittance transfer, according to World Bank data for 2025, is around 6.36% of the amount.

| Where the loss occurs | What happens | Why it matters to the operator |

|---|---|---|

| Rolling reserve | The acquirer holds back part of the turnover for a period of weeks to months | If the reserve sits in a weak currency, its real value falls |

| Settlement delay | Money moves through a cross-border chain for 1-3+ days | The rate can change before the funds are actually received |

| Pre-funding | Banks hold liquidity in the needed currencies in advance | Money is tied up before it is actually needed |

| Late FX conversion | Funds are converted not at the moment of deposit, but later | The final rate can be worse than expected |

Rolling reserve is not always a problem on its own. It becomes a problem when money sits for a long time in a currency that is losing value quickly.

Stablecoins are in demand where local currencies work less well

USD stablecoins are growing in the markets where there is inflation, currency restrictions and weak cross-border payments. The logic is simple: if the local currency is unstable and card payments are often declined, players and businesses need a more predictable settlement tool.

Stablecoins help operators reduce the time funds spend in a weak local currency and get a USD equivalent faster.

| What stablecoins help reduce | What they do not remove |

|---|---|

| Currency risk from local currency | Stablecoin issuer risk |

| Delays in some cross-border corridors | Compliance and sanctions screening |

| Dependency on card acquirers | Restrictions of specific jurisdictions |

| Losses from late FX conversion | Risk of stablecoin breaking its peg |

Stablecoins are not a bank deposit and do not remove all risks. But for an operator in emerging markets they can be a practical settlement tool if speed, a USD equivalent and less dependency on local currency are needed.

Volatile crypto needs to be kept separate from stablecoins

Accepting BTC or ETH as a deposit method and holding BTC or ETH on the balance are two different decisions.

The first gives the player a convenient payment method. The second creates market risk for the operator. If the BTC or ETH rate moves sharply, the financial result starts to depend not only on GGR and payment fees, but also on market movements.

Auto-conversion solves this operationally. The operator can accept volatile assets but automatically convert them into stablecoins when a set threshold is reached. This way crypto stays a deposit method, not an unplanned investment position on the balance.

Case study: operator with $150M turnover in 120+ markets

One of the operators working with Finassets is an online casino with a presence in more than 120 jurisdictions and annual turnover of around $150M (at the time of integration; operator data). Before integrating crypto processing, the platform only accepted fiat. As players started choosing crypto deposits more often, the operator began losing some new registrations to competitors who already had this option.

After integration, first results appeared within two weeks. Over the following months:

| Metric | Result |

|---|---|

| Active players who chose crypto as their main deposit method | 10x growth |

| Total deposit volume | 28x growth |

| GGR | Growth of up to 70% |

Auto-conversion was the key element. The operator set thresholds for volatile assets, and everything above those thresholds was automatically converted into stablecoins. This reduced manual work in treasury and made financial flows more predictable.

Results of a specific licensed operator. Individual outcomes may vary.

What changed in 2025-2026

Over the last 12 months, three trends have strengthened at the same time.

Stablecoins have grown in scale. BIS and IMF are recording growth in the number of active stablecoins, market capitalisation and cross-border volumes.

BTC volatility has become an important factor again. CME options data shows that BTC market risk remains significant. For an operator, this is an argument for auto-conversion if they accept volatile assets.

Cross-border friction remains. BIS and FSB show that G20 targets for speed and cost of cross-border payments have not yet been met. This is why alternative rails remain relevant for international operators.

Finassets: stablecoin processing and Auto-Convert

The losses described above appear in different places: rolling reserve in a weak currency, card friction on gambling MCC, market risk from BTC or ETH on the balance. Finassets covers these needs through a single payment setup.

Stablecoin acceptance and Auto-Convert

The operator can accept volatile assets and automatically convert them when a set threshold is exceeded. A stablecoin balance depends less on BTC or ETH movements.

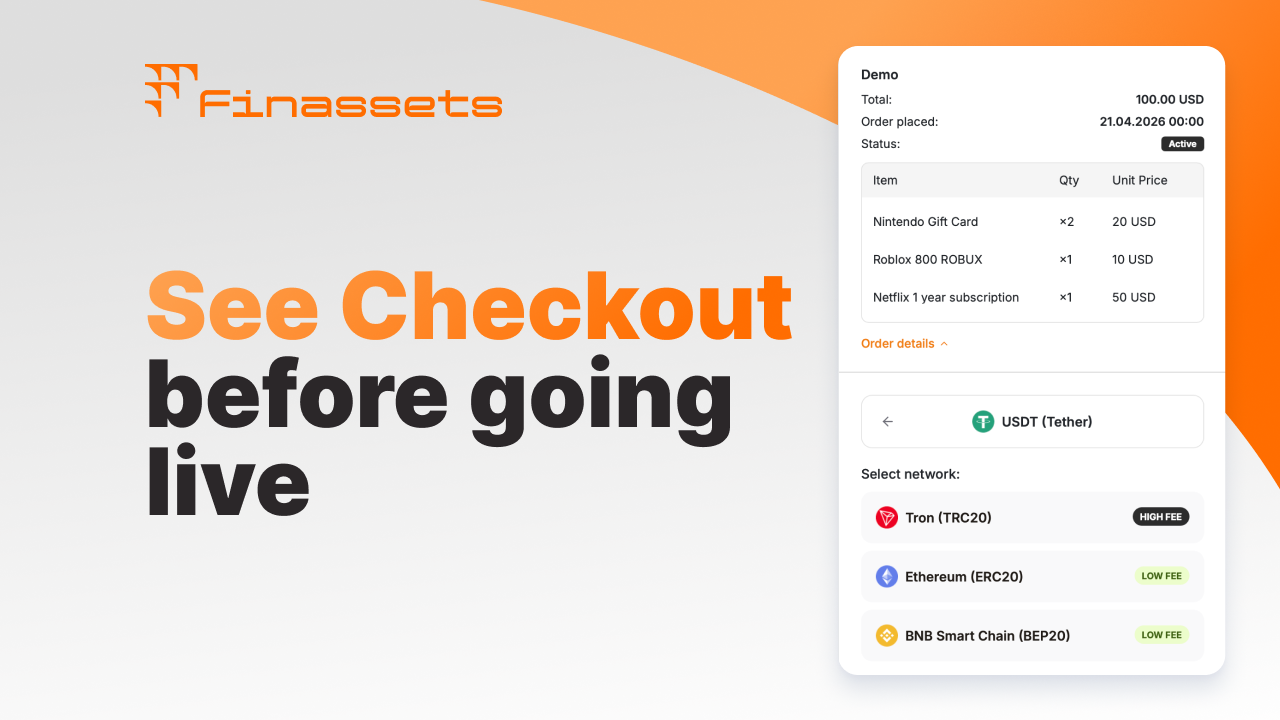

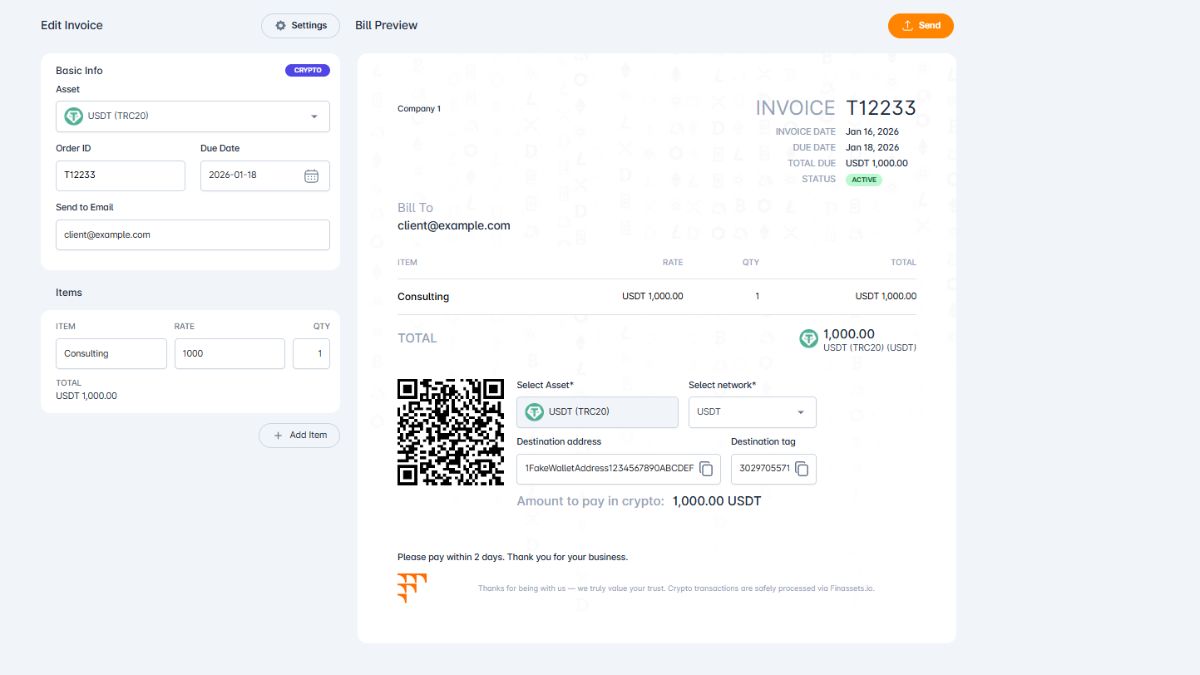

Structured Checkout

A unique address is created for each payment session. The transaction is immediately linked to the player and the deposit. The system supports partial payments, where one deposit is closed by several transfers in different assets.

TRON Energy Saving System

Pre-purchased Energy helps fix the cost of a TRC20 transfer before confirmation and can reduce the fee by more than 50% compared to the burn model. The effect depends on Energy availability and network conditions.

Pricing

Processing fee is calculated on a progressive scale 0.40% → 0.30% → 0.25% → 0.20% by volume. Other terms are fixed in the contract.

Regulatory status

Panama-registered B2B crypto payment infrastructure provider; supporting iGaming operators licensed under recognised regimes, including Curaçao, Anjouan, Kahnawake and others.

Onboarding

2-7 business days, subject to KYB and compliance review.

→ Go through the loss structure for your specific turnover

An iGaming operator's losses in emerging markets rarely come from one source. Rolling reserve is made worse by a weak currency. Card declines are linked to gambling MCC and cross-border routing. Volatile crypto on the balance adds market risk. Stablecoin processing with Auto-Convert helps reduce part of these losses where the problem is settlement delays, FX exposure and dependency on a card acquirer. Compliance remains mandatory throughout.

Get in touch with the Finassets team to go through which mechanisms are relevant for your market.