What the IMF’s New Data Standards Mean for Businesses

In December 2025, the International Monetary Fund published a departmental paper titled “Understanding Stablecoins”, prepared by its Monetary and Capital Markets Department.

The IMF is not a trend-chasing organization. As the world’s largest international financial institution and a specialized agency of the United Nations, it typically turns its attention only to phenomena that have reached systemic relevance. The fact that stablecoins are now the subject of deep IMF analysis is a signal in itself: stablecoins are no longer viewed as a niche crypto experiment. They are increasingly treated as a component of the global financial system.

This article looks at how the IMF frames stablecoins today, what risks and blind spots it highlights, and why new data standards are bringing stablecoins closer to regulated financial infrastructure — with direct implications for businesses.

CBDCs Are Still Catching Up to Market Reality

For years, central banks positioned central bank digital currencies (CBDCs) as the state’s answer to private digital money. In practice, progress has been slow.

According to the IMF’s overview:

- 85 out of 93 surveyed central banks are exploring CBDCs,

- yet only 3 countries have launched a retail CBDC,

- and many initiatives are delayed, slowed, or paused entirely.

Stablecoins, by contrast, scaled globally in a fraction of that time. They did so without legislative mandates, without central bank balance sheets, and without public-sector rollout cycles.

This rapid private-sector adoption is one of the reasons CBDC development accelerated in the first place. Stablecoins exposed a gap between how quickly digital money can spread and how slowly public institutions move to modernize payment infrastructure.

The Big Shift: Central Bank Backstops Enter the Conversation

One of the most consequential shifts in the IMF paper is conceptual rather than technical.

Regulators are no longer debating whether stablecoins should exist. Instead, they are discussing how regulated stablecoins might fit into the financial system under stress scenarios.

Authorities are now considering:

- whether certain regulated stablecoins could gain access to central bank liquidity facilities,

- and whether emergency backstop mechanisms should exist during periods of market stress.

These discussions come with strict conditions:

- robust regulation,

- transparent and high-quality reserves,

- clear supervisory oversight.

Once central bank backstops are even hypothetically on the table, stablecoins stop looking like speculative tokens. They start to resemble payment and settlement infrastructure, subject to many of the same expectations as traditional financial institutions.

Why Stablecoins Create System-Level Risk

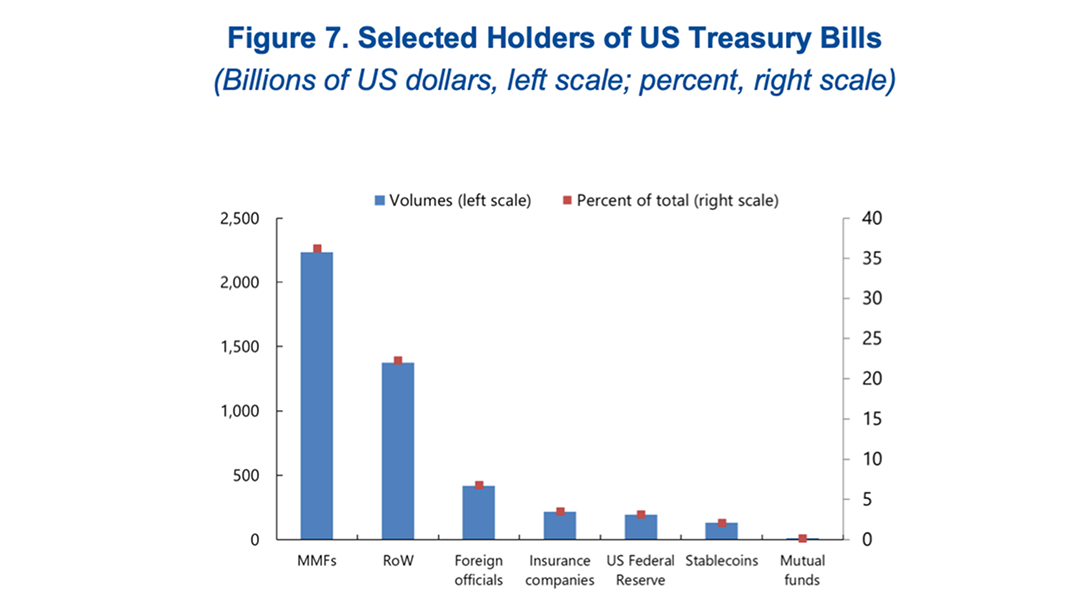

Today, stablecoins are still not a dominant payment method for the real economy. However, the IMF highlights a critical asymmetry: adoption is accelerating much faster than regulatory frameworks and data infrastructure.

While stablecoins currently hold only a limited share of the U.S. Treasury bill market, their absolute scale already places them alongside large institutional investors. Continued growth could begin to influence:

- government bond markets,

- short-term funding conditions,

- and liquidity dynamics during stress events.

This is not framed as an imminent crisis, but as a classic systemic risk pattern: something becomes important quietly, before institutions fully adapt.

A Blind Spot in the Financial System: Data

Perhaps the most striking finding in the IMF paper is not about liquidity or reserves, but about information.

Modern economic policymaking depends on data:

- who holds money,

- where it is held,

- how it moves across borders,

- and which sectors are exposed.

Stablecoins break many of these assumptions.

In many cases:

- issuers do not know who ultimately holds the coins,

- user residence and country exposure are opaque,

- distinctions between households, firms, and intermediaries blur.

When large volumes of money move globally without clear attribution, economic decision-making becomes harder — and riskier.

Why Stablecoins Are Hard to Measure

A common misconception is that blockchains are “fully transparent.” Technically, transactions are public. Economically, however, visibility remains limited.

The IMF highlights several consequences:

- balance of payments statistics become less reliable,

- monetary aggregates lose accuracy,

- cross-border capital flows are harder to interpret.

Stablecoins move freely across jurisdictions, but economic borders still matter for policy, taxation, and financial stability. The mismatch between technical transparency and economic insight is one of the core challenges regulators are now addressing.

What Regulators Are Doing About It: New Data Standards

In response, the IMF and the G20 launched Data Gaps Initiative 3, a new framework aimed at closing these blind spots.

Its goals include:

- identifying who holds stablecoins,

- measuring cross-border exposure,

- understanding systemic concentration risks.

The approach combines:

- harmonized reporting templates,

- issuer and intermediary disclosures,

- on-chain analytics,

- and international data sharing between authorities.

This marks a decisive shift. Stablecoins are increasingly treated not as peripheral crypto assets, but as components of the global financial architecture that must be observable, measurable, and governable.

What This Means for Businesses

For businesses, this regulatory evolution changes the calculus.

Stablecoins are moving toward:

- clearer compliance expectations,

- better-defined reporting standards,

- and closer integration with the regulated financial system.

That makes them more viable not just for crypto-native firms, but for companies looking to modernize payments, treasury operations, and cross-border settlements without stepping outside regulatory boundaries.

How Finassets Fits In

Businesses can already integrate cryptocurrencies and stablecoins into their operations today — provided they do so with the right infrastructure partner.

Finassets offers:

- deep expertise in crypto finance and payment processing,

- continuous alignment with evolving regulatory standards,

- secure, compliant infrastructure designed for global scale.

As stablecoins move closer to the core of the financial system, the question for businesses is no longer if they matter — but how to use them responsibly and efficiently.

👉 Grow your business with Finassets — possibly the best stablecoin payment gateway in the industry.