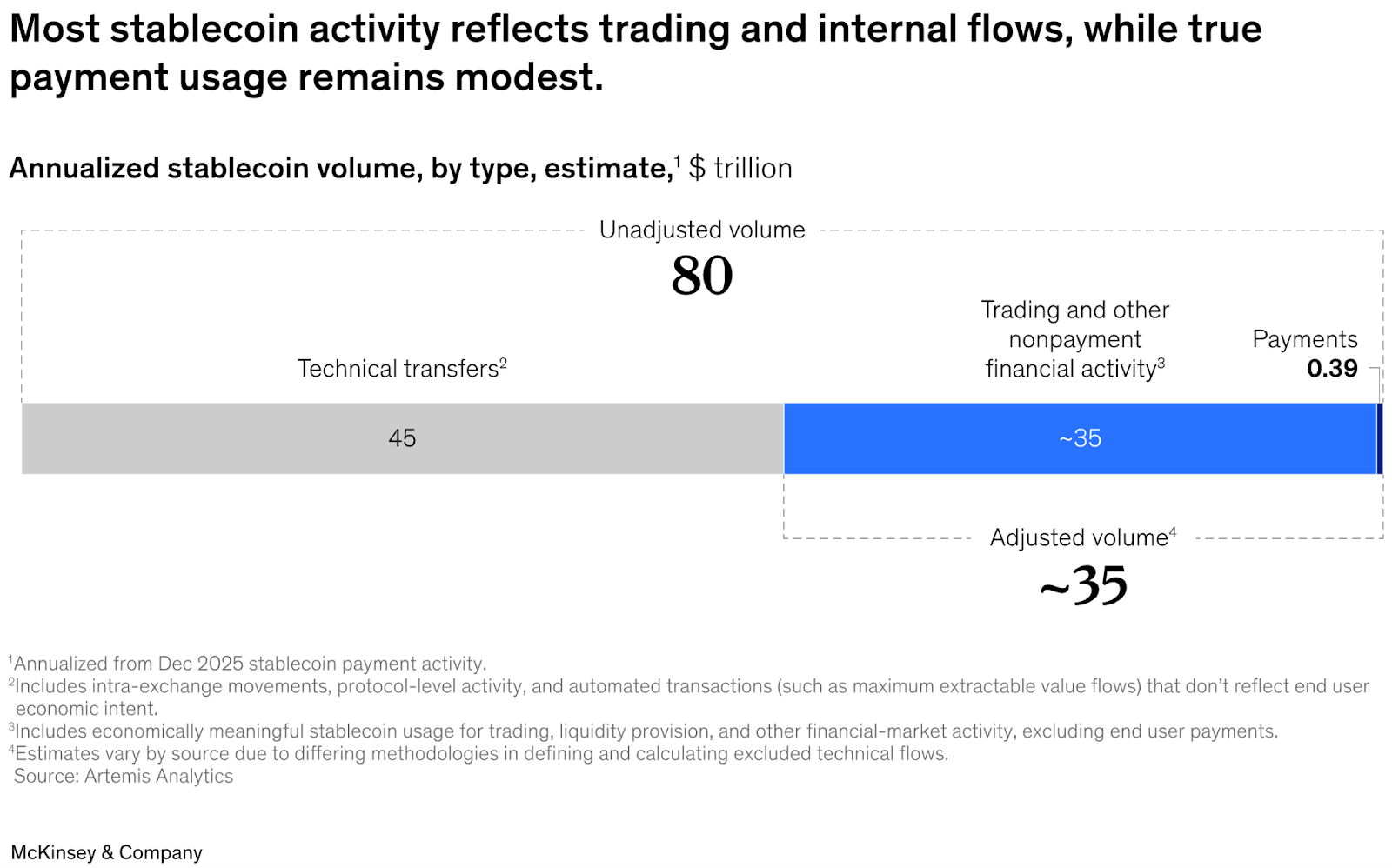

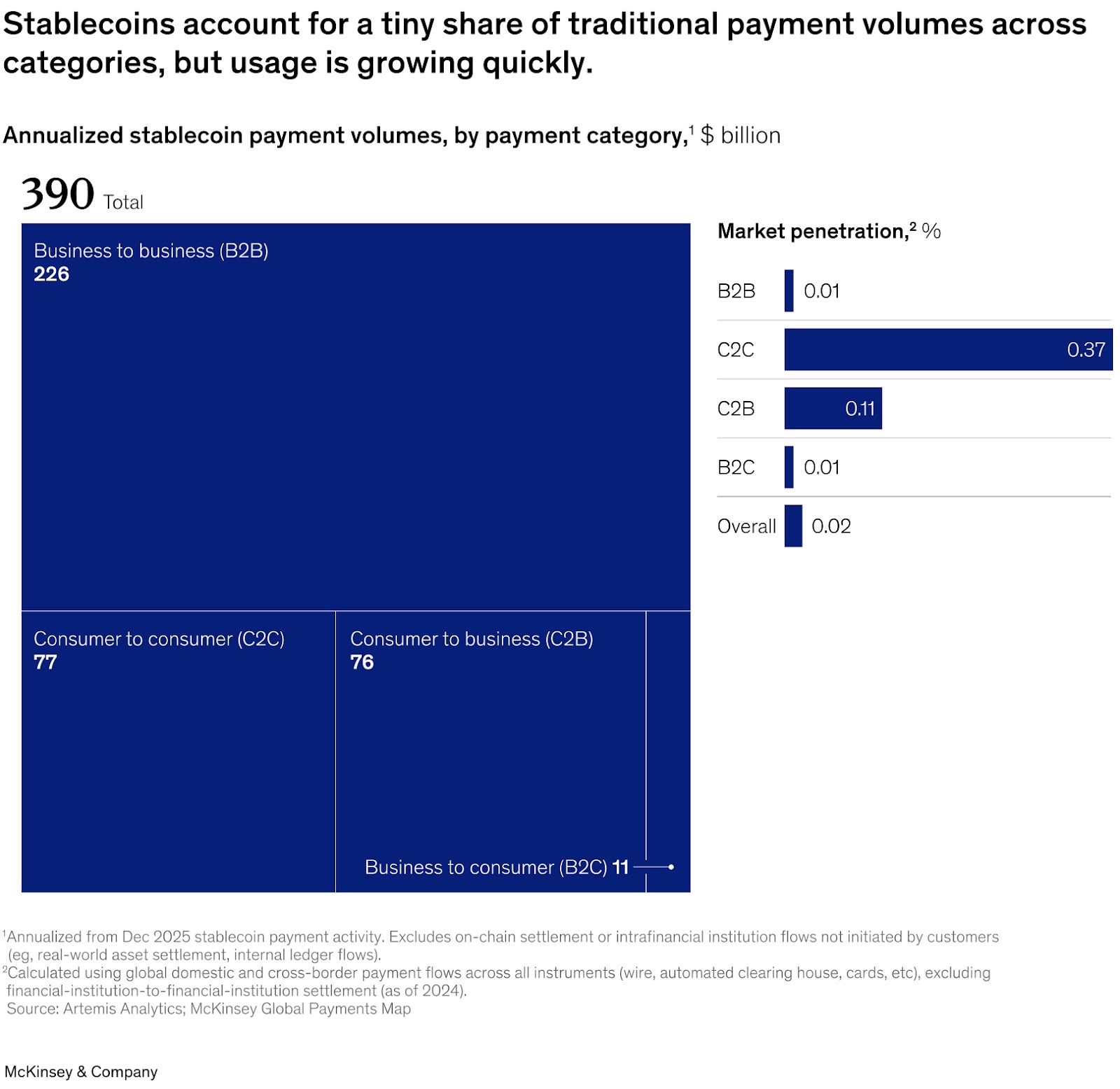

On February 18, 2026, McKinsey published “Stablecoins in payments: What the raw transaction numbers miss.” Headline figures often mention trillions of dollars in stablecoin volume. Those numbers reflect total on-chain activity. When trading flows, internal transfers, and automated transactions are filtered out, the annual volume of real payments is closer to $390 billion. Around 60% of that comes from B2B transactions.

B2B stablecoin payments also grew 733% year over year in 2025. This shows where real usage is expanding. Retail crypto payments are still developing. Business payments are already integrating stablecoins into daily operations.

B2B adoption is driven by operational efficiency

Retail adoption depends on consumer habits. Cards and mobile wallets already work well for most shoppers. A new payment method must feel simple and familiar before it can scale.

B2B payments follow a different logic. Companies focus on speed, liquidity, and cost control. When settlements take several days, working capital is tied up. When cross-border wires pass through multiple banks, fees and delays increase.

Stablecoins reduce settlement time and operate around the clock. They move value across borders without relying on long banking chains. For treasury teams, this improves predictability and cash flow management.

Stablecoins are solving concrete cross-border problems

McKinsey estimates that B2B stablecoin payments account for roughly $226 billion per year. This is still a small share of global B2B volumes, yet growth is strong.

Companies are using stablecoins for:

- cross-border supplier payments

- international service contracts

- marketplace settlements

- transfers between subsidiaries

Stablecoins are increasingly treated as infrastructure for specific payment corridors.

High-risk and offshore sectors are early adopters

Industries like iGaming and digital services often face banking restrictions. Payments get delayed, accounts are reviewed, and cross-border transfers slow down operations. Offshore companies deal with even more complexity across different regions.

Stablecoins help maintain continuity by reducing reliance on a single bank and enabling faster international payouts. When working with licensed and regulated partners such as Finassets low-fee crypto payment gateway, businesses can use crypto within a compliant framework across multiple jurisdictions.

Retail adoption requires broader ecosystem alignment

Retail crypto payments depend on merchant integration, consumer education, and regulatory clarity. Stablecoin-linked cards are expanding usability by allowing digital balances to be spent through established card networks.

Retail change usually takes time because it involves millions of users adjusting behavior.

B2B change can happen faster. A finance team can pilot a new settlement method within one region or product line. Results can be measured directly in lower fees or faster settlements. When benefits are clear, expansion follows.

Stablecoins are becoming part of B2B payment infrastructure

Stablecoins are not replacing banks. Most businesses convert them into fiat after settlement, while licensed providers manage compliance and risk controls.

The change is happening at the settlement layer. In specific industries and cross-border corridors, stablecoins act as efficient digital cash.

If you are exploring how to integrate crypto payments into your business, contact the Finassets team to start using crypto in your operations.